China's Monopoly in the Rare Earth Metals Industry

(Yanina Chaikivska, analyst, journalist)

Over the past three years, whenever Washington begins to restrict technology transfer or increases tariffs for Chinese goods, Beijing has retaliated by ramping up economic pressure on the United States’ defense-industrial base. China wields significant leverage in this confrontation: a near-total monopoly on the extraction and processing of rare earth metals (REMs).

China’s Global Domimance

According to the Center for Strategic and International Studies (CSIS) [5], China currently accounts for 60% of the global rare earth metal production. China has a real monopoly in the processing of these metals, which is 90%. Therefore, China imports rare earth metals from other countries [5]. If we break down these figures, China refines 89% of the world’s neodymium and praseodymium. These metals play a major role in the manufacture of electromagnets. According to the forecasts of the consulting company Benchmark Mineral Intelligence, by 2028, Chinese production of rare earth elements will decrease to 75% [8].

The article “Mine the Tech Gap: Why China’s Rare Earth Dominance Persists” mentions that China has a monopoly on the processing of such heavy rare earth metals as dysprosium (Dy) and terbium (Tb), and light rare earth metals as neodymium (Nd) and praseodymium (Pr) [7].

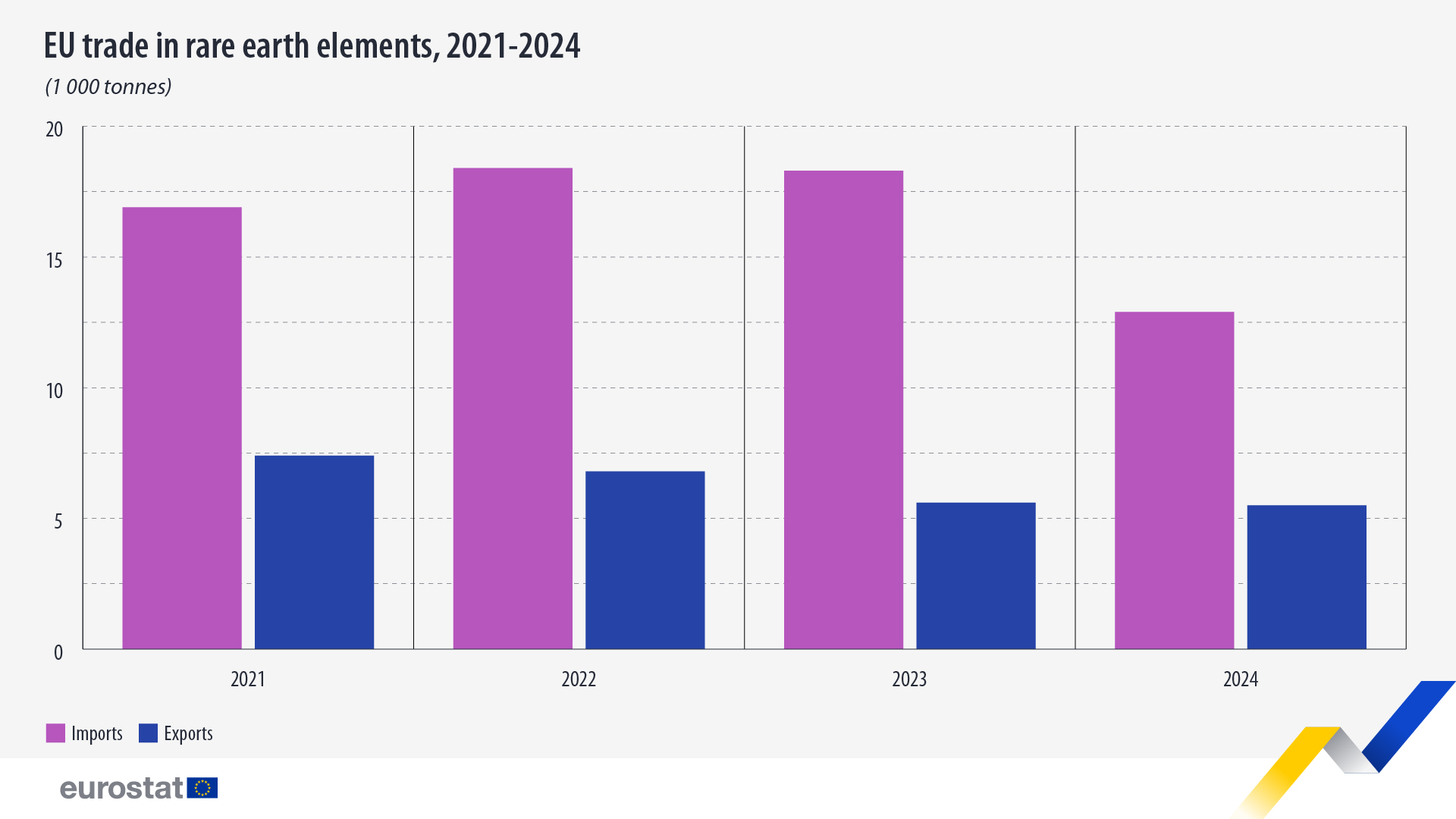

The European Commission website published information that in 2024, 12,900 tons of rare earth elements were imported into the EU, which is 29.3% less than in 2023. At the same time, 5,500 tons of rare earth elements were exported from the EU. Overall, the drop in exports was only 0.8%.

Trade of rare earth elements during 2021-2024 (Source: European Commission website).

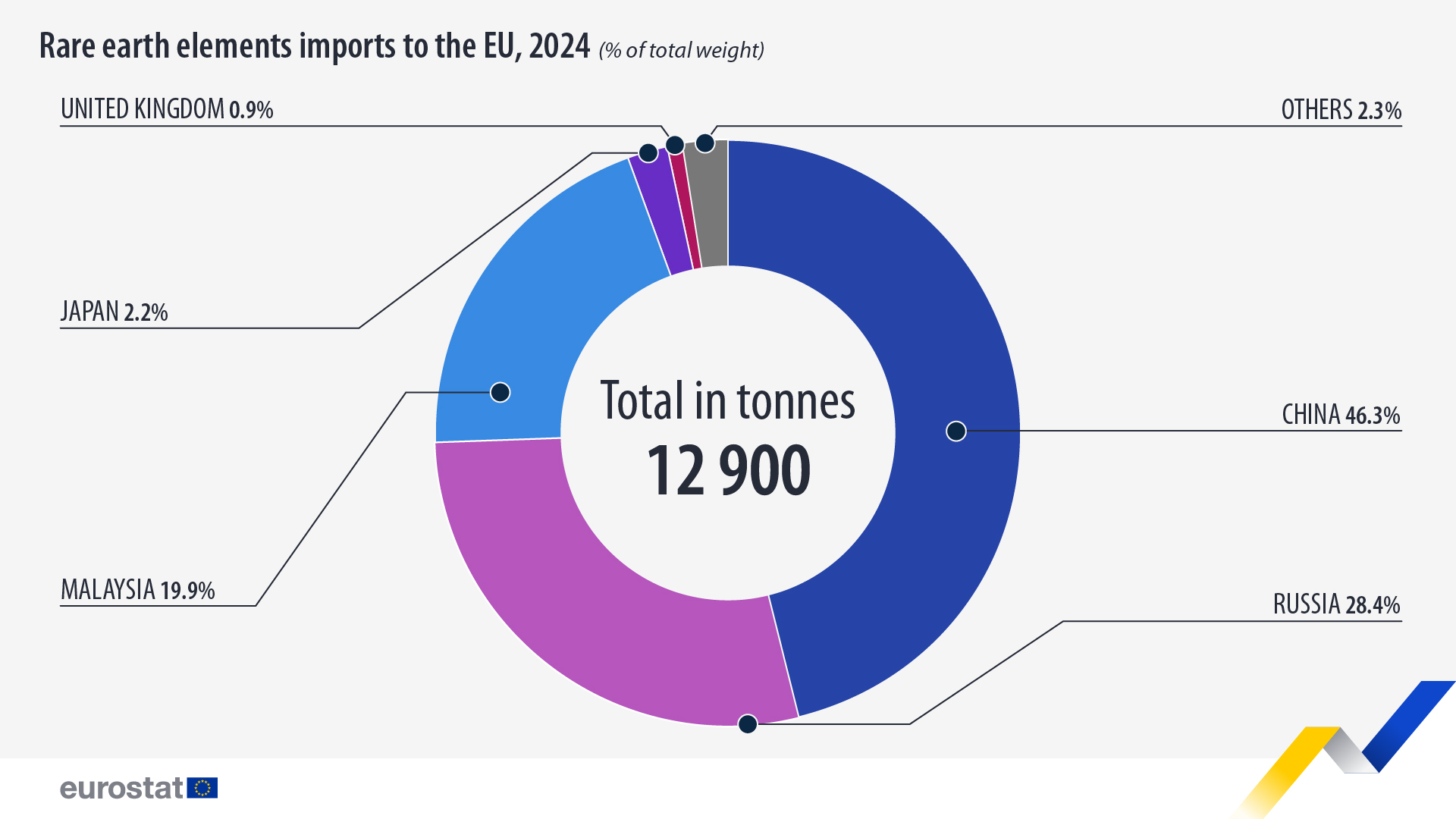

Almost half of rare earth imports came from China in 2024, accounting for 46.3% of total imports (6,000 tonnes). Russia is in second place with 28.4% of imports (3,700 tonnes), and Malaysia is in third place with 19.9% of imports (2,600 tonnes) [39].

EU imports of rare earth elements in 2024 (Source: European Commission website).

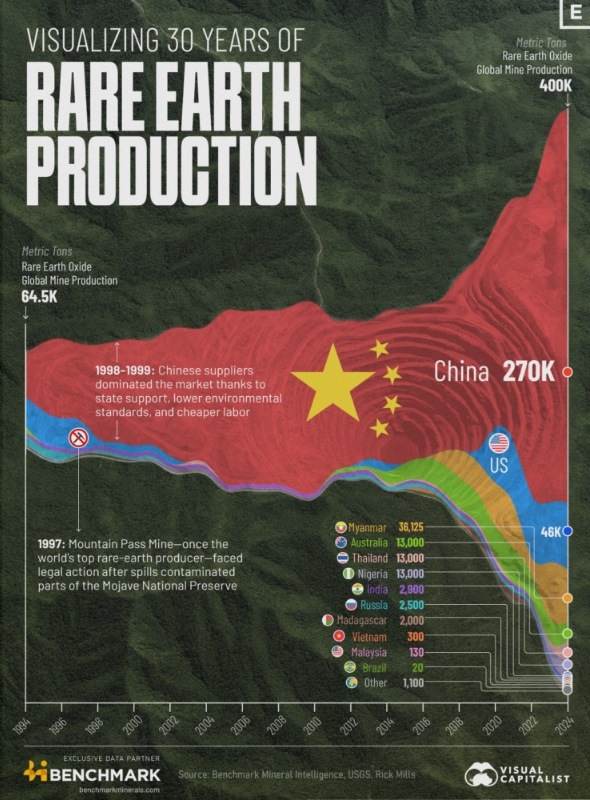

In 2024, rare earth metal production increased to 390,000 metric tonnes worldwide [41]. There was also an increase in demand for neodymium, dysprosium, praseodymium and yttrium, which is associated with the rapid development of technology. In 2024, 70% of rare earth imports to the United States came from China. The United States is the second largest producer of rare earth elements, but it lags behind China. At the same time, rare earth reserves in the United States account for only 2% of the total world reserves [41]. Russia produced only 2,600 tons of rare earth elements in 2024. This figure has been stable for the past five years, which indicates a lack of development of this industry in the Russian Federation.

Source Daily Economy.

According to the United States Geological Survey (USGS), published in the article “Top 10 Countries by Rare Earth Metal Production” [41], the top ten countries by rare earth metal production in 2024 are:

1. China. In 2024, China’s domestic production of rare earth elements was 270,000 metric tons, compared to 255,000 metric tons in 2023.

2. United States. The United States produced 45,000 metric tons of rare earth elements in 2024, compared to 41,600 metric tons in 2023 (the main mine is Mountain Pass in California, owned by MP Materials, which produces high-purity neodymium and praseodymium oxide). The US Geological Survey estimates the value of rare earth imports to the US in 2024 at \$170 million, down from \$186 million in 2023.

3. Myanmar. REM production in 2024 was 31,000 metric tons of rare earths. Myanmar saw a 27% decline in production. This is due to instability in the country following a military coup in 2021.

4. Australia. REM production in 2024 was 13,000 metric tons, down from 16,000 metric tons in 2023. Australia has the fourth-largest reserves of rare earths in the world and is poised to increase its production. Lynas Rare Earths is the leading REE producer outside of China, operating the Mount Weld mine and concentrator in Western Australia.

5. Nigeria. Nigeria’s rare earth production in 2024 was 13,000 metric tons, up more than 80% from 2023. In late 2024, the Nigerian government signed a memorandum of understanding with the French government to jointly develop critical minerals including REE.

6. Thailand. Its REE production in 2024 was 13,000 metric tons, up 261% from 2023. The country is China’s main source of rare earth imports. Neo Performance Materials' subsidiary Neo Magnequench controls a rare earth magnetic materials manufacturing facility in Korat. Chinese electric vehicle giant BYD opened a \$486 million electric vehicle manufacturing facility in Thailand in July 2023. According to the Financial Times, this will further expand Chinese electric vehicle manufacturers' reach into Southeast Asia.

7. India. India’s REE production in 2024 was 2,900 metric tons, unchanged from the previous few years. India’s REE production is well below its potential. This is despite the country having 35% of the world’s total beach sand deposits, which are sources of REE.

8. Russia. Russia produced 2,600 metric tons of REE in 2024, the same as it has over the past five years. Russia ranks fifth in the world in terms of REE reserves. Russia’s largest REE deposit is Tomtor (developed by TriArk Mining). It is a joint venture between the industrial conglomerate Rostec and billionaire Alexander Nesis.

9. Madagascar. Madagascar produced 2,000 metric tons of rare earth elements in 2024, almost on par with 2,100 metric tons in 2023, but significantly less than the 6,800 metric tons in 2021. The Ampasindava Peninsula contains 628 million metric tons of ionic clays with significant concentrations of rare earth elements. This is one of the largest REE deposits outside of China.

10. Vietnam. Rare earth element production in 2024 was 300 metric tons, the same as in 2023. This is 75% less than the 1,200 metric tons in 2022. Vietnam has the sixth largest reserves of rare earth elements in the world, including deposits on the northwestern border with China and along the east coast.

According to CSIS experts [5], China has a number of advantages in the extraction of rare earth metals compared to other countries. These advantages are:

- the availability of technical know-how in the field of processing and purification of rare earth metals;

- in other countries, plants for the separation, processing and production of rare earth metals are under construction, so it will take many years to complete and put into operation;

- the extraction and processing of rare earth metals harm the environment. Western countries are not ready to take these risks [5].

Rare Earth Resources of the PRC

According to Reuters, the reserves of rare earth metals in the PRC are 44 million metric tons, which is 34% of the total world reserves [8]. The most famous among them are heavy REEs, the total amount of which reaches 80% of the world reserves of heavy rare earth metals. They are mined in several regions of the PRC.

In the north of China, the main producer of rare earth metals is Inner Mongolia Baotou Steel Rare-Earth Hi-Tech Company, in the south - China Minmetals. Other large companies are Aluminum Corporation of China Limited and China Non-Ferrous Metal Mining. There are also two state research institutions in China that specialize in the study of rare earth elements, in particular, the State Laboratory of Chemistry and Application of Rare Earth Materials, affiliated with Peking University, and the State Laboratory for the Utilization of Rare Earth Materials Resources in Changchun (Jilin Province).

Deposits of the PRC:

– the largest deposit is located in Bayan-Obo in Inner Mongolia (accounting for more than 50% of the world's production of rare earth metals and 70% of the reserves of these metals in China. According to the Voice of America, the largest rare earth mining company in this region is China Northern Rare Earth High-Tech [10]);

– large deposits have been developed in Sichuan Province, Weishan District in Shandong Province;

– in the Xinjiang Uyghur Autonomous Region there are large veins of pegmatites in the deposits of Kyoktokai, Kuzhurti, Khusti, Obogon, Bazai;

– pegmatite deposits in Guangdong Province (near Changzhou);

– the Yichun tantalum deposit is in Jiangxi Province;

– from 10 to 20 tons of tantalum are mined at the Limu enterprises (Guangxi Zhuang Autonomous Region);

– lithium is mined from salt lakes in central and western China, as well as from pegmatites in the Shanpi deposit (Jiangxi province) and Dangsimu (Inner Mongolia);

– in 2024, several new large deposits were discovered in China: in Yunnan province [15]. According to information in Chinese media, they may have more than 1.15 million tons of resources [16]. A press release from the China Geological Survey (CGS) indicated that the deposit may be a source of praseodymium, neodymium, dysprosium and terbium and contain more than 470,000 tons of these minerals [16];

– in July 2024, Chinese geologists discovered two new minerals, oboniobite and scandium-fluorine-eckermanite, in the Bayan-Obo mine in Inner Mongolia [16].

In 2022, China Northern Rare Earth Group announced that its subsidiary Zibo Baosteel Lingzhi Rare Earth High-tech Co., Ltd., a 25,000-ton-per-year rare earth chloride smelter in Zibo, Shandong Province, East China, had completed construction and passed testing. The company specializes in rare earth polishing powder, which is composed of cerium oxide. The demand for it is high due to the rapid growth of demand for electronic products, including mobile phones and liquid crystal displays [26].

Shandong Shenghe New Materials Technology Co., Ltd. produces 5,500 tons of rare earth elements annually and transfers them to the park for Zhongkai rare Earth Materials Co., Ltd. Zhongkai rare Earth Materials Co., Ltd. Shandong Shenghe New Materials Technology Co., Ltd. is located in Hanjia Village and Xiuwang Village, Jinshan City [27].

Sichuan has established a national rare earth production base with an industrial scale of rare earth elements of over 1.474 billion US dollars by 2027. Sichuan has accelerated the restructuring and integration of rare earth mines in Mianning and Dechang. Rare earth elements are smelted and separated in Leshan and Liangshan. Chengdu, Mianyang, Leshan are developing the deep processing industry of rare earth metals [27].

Jiangxi Rare Earth & Rare Metals Tungsten Group Imp & Exp Co., Ltd. is a subsidiary of Jiangxi Rare Metals Tungsten Group Holding Co., Ltd. It is one of the large industrial conglomerates in Jiangxi Province and is focused on tungsten production. JXHC is a large state-owned industrial enterprise in China with sales revenue of over 10 billion, which has nine tungsten mines in China with a total tungsten concentrate capacity of nearly 10,000 tons per year, as well as more than eight factories with a total production capacity of about 30,000 tonnes [27].

“Rare” REM or the miracle of Chinese monopoly

The name “rare” is not due to the fact that these metals are rare. In fact, there are more of them than silver and gold. China’s dominance in this industry is due to the fact that the extraction and purification of these metals are environmentally destructive to the environment. China did not care about the state of the environment, so it developed its capacity to become a monopolist. The US and other Western countries have been willing to send their rare earths to China for refining so as not to create an environmental disaster [29].

If Beijing continues to use its monopoly as leverage, Western countries, including Japan, are ready to seek alternatives and develop processing methods that are much more environmentally friendly. Japan has already suggested that the G-7 (Canada, France, Germany, Italy, the UK and the US) join forces to find and fund methods for extracting and processing rare earths in Africa and Latin America. Japan is ready to take the lead in creating alternatives [29].

The US has begun supporting the domestic rare earth value chain by funding research and projects under the Inflation Reduction Act. Australia supports rare earth projects through tax breaks, and Europe is seeking to increase supplies through domestic supply quota targets. The Australian budget for 2024-2025 included a 10% mining tax credit and funding for pre-feasibility studies for all critical minerals, including rare earths. The Biden administration in the United States has imposed a 25% import duty on rare earth magnets from China from 2026.

Global reserves are estimated at around 115 million tonnes. This is enough to last the world for 300 years. More deposits are likely to be discovered in the coming years, so resource scarcity is not a problem [32].

In 2024, a Norwegian mining company announced that it had discovered Europe’s largest explored rare earth deposit not owned or controlled by China. The discovery by Rare Earths Norway was a boost to Europe’s efforts to challenge China’s dominance in the rare earths industry.

On July 10, 2025, Donald Trump met with five West African leaders at the White House to discuss trade and development, and to increase the American presence on the African continent. Trump emphasized the US desire to conclude trade agreements on rare earths to reduce dependence on China. This could counterbalance China's traditional "infrastructure for resources" strategy.

China is concerned about securing its domestic market

The growth of domestic demand and prices has prompted Chinese exporters to sell more REEs domestically. As a result, in September 2024, exports of rare earth minerals from China fell by 11.5% compared to August [31]. China is rapidly growing in the production of electric vehicles and consumer electronics, the production of which requires rare earth metals. “Some exporters preferred to sell domestically against the backdrop of rising prices,” said Yang Jiawen, an analyst at Shanghai Metals (SMM) Market consulting company. On September 30, 2024, spot prices for praseodymium-neodymium oxide in China increased by 5% compared to August of the same year. This is due to the fact that the Chinese government introduced new regulations for the industry from October 1, so the extraction of REEs was lower than expected. Smelting and separation quotas and increased seasonal demand played a role. All of this has combined to reduce domestic supply and increase prices. At the same time, interest in magnetic products abroad has waned as supply outside China has increased.

Four rare earth elements are of particular importance to modern technology -neodymium, praseodymium, dysprosium, and terbium. They are expected to account for 98% of the rare earth market by 2030.

Neha Mukherjee, senior analyst for critical minerals at Benchmark Mineral Intelligence [31], said the country of a billion people can maintain its dominance in the industry because of its economic scale, government subsidies, and vast reserves. These factors help to keep rare earth prices in China more competitive than in other countries. China is focused on maintaining stable rare earth prices to support its domestic electric vehicle industry.

China's manufacturing sector is now larger than the US, Germany, Japan, South Korea and the UK combined. China is close to ending its dependence on US supplies in many sectors, with the exception of the fastest semiconductors.

China is developing and mining rare earth metals in other countries, but without Russia

China is actively increasing imports of rare earth raw materials in the form of unseparated compounds from other countries. In 2021-2023, Vietnam exported 3.4-3.6 thousand tons of rare earth products to China [34].

Malaysia has built a hydrometallurgical plant LAMP, which produces neodymium and praseodymium. Products are supplied to Japan, France and China, with China's share in 2022 being 36% [34].

In early 2025, China’s imports of rare earth elements fell by 41.1% compared to 2023 to 9,645 tons. In 2024, 132,931 tons were produced, which is 24.4% less than in 2023. Experts believe that the drop was due to reduced supplies from the United States and Myanmar [18].

In October 2024, military groups fighting the military regime in Myanmar took control of a mining center that is a major supplier of rare earth oxides to China. This caused the supply to stop [18].

Imports of heavy rare earth oxides from Myanmar to China grew rapidly from 19,500 tons in 2021 to 41,700 tons in 2023. The latter figure is more than double China’s own quota for domestic rare earth mining. Satellite images analyzed by Global Witness have shown significant destruction in Myanmar due to this mining. In Kachin 1, which is controlled by armed groups linked to the Myanmar government, the number of mining sites has increased by 40%. This mining covers an area from the border town of Pangwa to Chipwe. An increase in mining sites has also been observed in Momauk, a region controlled by the Kachin Independence Organization. The vast majority of mining in the country is illegal and controlled by illegitimate military militias [6].

Trade data shows that most of the chemicals for mining come from China. In 2023, 1.5 million tons of ammonium sulfate and 174,000 tons of oxalic acid were exported to Myanmar [6].

China receives 70% of its raw materials for medium and heavy rare earth metals from Myanmar, including dysprosium and terbium. The extraction of these metals is critical for clean energy technologies (electric vehicles and wind turbines) [10].

According to London-based Benchmark Mineral Intelligence [11], Chinese companies control most of the cobalt mines (important for electric vehicle batteries) in the Democratic Republic of Congo. Congo accounts for 70% of the world’s cobalt supply.

Professor Zuo Zhengguang [35] of the Laboratory of Geological Processes and Mineral Resources at the China University of Earth Sciences and his team are working to use artificial intelligence technologies to pinpoint the exact coordinates of rare earth deposits in the Himalayas. According to preliminary estimates, this may be a belt over a thousand kilometers long in the highlands near the southern borders of Tibet. This is a disputed territory between China and India. In China, these metals are important for the production of electric vehicles, electronic devices, batteries, wind turbines, efficient oil refining, and the military-industrial complex. President Recep Tayyip Erdoğan met with President Xi Jinping in Kazakhstan in July 2024 [30] to discuss cooperation in the development of REE. In 2022, Turkey discovered that it has a large reserve of rare earth elements in Beylikduzu near Eskisehir in central Anatolia. The Ministry of Energy Turkey has announced its readiness to build a plant there to process the raw materials. At the same time, the Chinese Communist Party newspaper Global Times wrote that “this discovery has created an opportunity for China and Turkey to cooperate.”

Strategic advantages of China’s rare earth monopoly

China’s dominance in the rare earth industry is no accident; it is the result of decades of strategic planning, technological investment, and economic maneuvering. Control advantages [17]:

1. Cost advantages. China has used its low labor costs, government subsidies, and less stringent environmental regulations to produce rare earths at a fraction of the cost of other countries.

2. Processing capabilities. The most critical bottleneck in the rare earth supply chain is not mining, but processing.

3. Vertical integration of the supply chain. This allows China to control not only raw materials but also valuable products derived from rare earths, such as magnets and advanced alloys used in the technology and defense industries.

4. Global influence through export policy.

5. Critical role in green energy and technology. Rare earth metals are essential for renewable energy technologies such as wind turbines, electric vehicle engines, and solar panels.

6. Economic and geopolitical leverage. In today’s world, geopolitical tensions are moving beyond traditional battlefields and into the economic and technological realms. One of the most powerful tools in this confrontation is control over the supply chains of critical raw materials. China’s dominance in rare earths gives it unprecedented leverage over the economies and defense sectors of the United States and the European Union. This dependence turns raw materials into weapons that can destabilize Western democracies without firing a shot [40].

Scenarios for China’s Pressure on Other Economies

In the article “Caught in the US-China Crossfire: To Protect Itself, Europe Must Call a Critical Raw Material Emergency” [40] provides a detailed analysis of the global threats posed by China to its dominance in the extraction and refining of rare earth elements. The authors propose three potential scenarios for Beijing to use its monopoly on critical materials to pressure the democratic alliance.

Scenario 1: A targeted attack with unpredictable consequences

China seeks to cause chaos. Beijing threatens to impose sanctions on component manufacturers from third countries, in particular South Korean companies that produce transformers and supply products to the US military. In addition, the PRC may block supplies to European wafer manufacturers in order to disrupt production processes in the US military-industrial complex. The threat to global security is that China has become the largest semiconductor manufacturer and is rapidly increasing production of all types of chips. At the same time, the US and the EU still do not produce gallium.

Scenario 2: An untargeted attack with major consequences

Assuming that China’s goal is to deal the strongest possible blow to the US military, it needs to drastically reduce or stop exports to other countries. Even reducing supplies already has many threats. For example, a 30% reduction in gallium exports could reduce US economic output by US\$602 billion (2.1% of GDP). Such actions could destroy American and European industry, which would lead to a weakening of deterrence in Europe and Asia.

Scenario 3: Attack from several fronts

China has modernized its armed forces, expanded military exercises near Taiwan, and intensified military activity in the “gray” zone. If a diplomatic conflict or military confrontation occurs between the United States and China, the PRC may stop exporting critical raw materials. In this case, China will use all means at its disposal, including material dependence, to sabotage the attempts of the United States and its allies to mass produce new weapons systems [40].

Europe will face various risks, since in the event of the United States being involved in a conflict in East Asia, the priority for the supply of scarce ammunition and weapons systems will be directed to the Indo-Pacific region. Experts argue that the United States and the EU should prepare for the worst.

Conclusions

China will maintain an undisputed monopoly on the rare earth metals (REE) market in the coming years and will do everything possible to prevent other countries from shaking its position. Thanks to its monopoly, the PRC gains economic and geopolitical leverage over the economies and defense sectors of the US and the European Union, turning raw materials into weapons.

The West, for its part, will continue to look for ways to protect itself from Chinese hegemony in the REE sector. We can already see this today in the example of the US. All previous steps by the EU, Australia and the US indicate that these countries are making efforts to diversify sources of supply and reduce geopolitical risks. India, which has significant reserves of REE and is a democratic state, in whose interests there is also a need to weaken Chinese influence, could become a very important player here.

References

1. Кирило Овсяний, Анна Миронюк. Як Китай забезпечує воєнну машину РФ критично важливими рідкісними металами (розслідування). 30 січня 2025. https://www.radiosvoboda.org/a/skhemy-kytay-rosiya-metaly-stybiy-haliy-hermaniy/33297483.html

2. Rare earth elements facts https://natural-resources.canada.ca/minerals-mining/mining-data-statistics-analysis/minerals-metals-facts/rare-earth-elements-facts

3. William Clarke. The West's critical mineral policy is putting the cart before the horse. It's not a supply problem, it's a demand problem. 16 August 2024 https://www.mining-journal.com/energy-minerals/opinion-articles/4347749/wests-critical-mineral-policy-putting-cart-horse?&utm_campaign={campaignname}&utm_content={adgroupname}&utm_term=china%27s%20mining&device=c&position=&matchtype=p&network=g&gad_source=1&gclid=EAIaIQobChMIscDe4r3PiwMVzTIIBR28uzI3EAAYASAAEgLlbPD_BwE

4. https://en.wikipedia.org/wiki/Rare_earth_industry_in_China

5. Gracelin Baskaran. What China’s Ban on Rare Earths Processing Technology Exports Means. January 8, 2024 https://www.csis.org/analysis/what-chinas-ban-rare-earths-processing-technology-exports-means

6. Fuelling the future, poisoning the present: Myanmar’s rare earth boom. 23 May 2024. https://globalwitness.org/en/campaigns/transition-minerals/fuelling-the-future-poisoning-the-present-myanmars-rare-earth-boom/

7. Nayan Seth. Mine the Tech Gap: Why China’s Rare Earth Dominance Persists. https://www.newsecuritybeat.org/2024/08/mine-the-tech-gap-why-chinas-rare-earth-dominance-persists/

8. Mai Nguyen and Eric Onstad. China's rare earths dominance in focus after it limits germanium and gallium exports. December 21, 2023 https://www.reuters.com/markets/commodities/chinas-rare-earths-dominance-focus-after-mineral-export-curbs-2023-07-05/

9. China Dominates the Rare Earths Market. This U.S. Mine Is Trying to Change That. https://www.politico.com/news/magazine/2022/12/14/rare-earth-mines-00071102

10. Melissa Pistilli. Top 11 Countries by Rare Earth Metal Production. Aug. 29, 2024 https://investingnews.com/daily/resource-investing/critical-metals-investing/rare-earth-investing/rare-earth-metal-production/

11. Saibal Dasgupta. China may use rare earth to retaliate against US, say analysts. December 09, 2024. https://www.voanews.com/a/china-may-use-rare-earth-to-retaliate-against-us-say-analysts/7892877.html

12. Що відомо про рідкісноземельні метали в Україні. 4 Лютого 2025, 11:56 https://kyiv24.news/news/shho-vidomo-pro-ridkozemelni-metaly-v-ukrayini

14. Микола Топалов , Богдан Мірошниченко. Метали в обмін на безпеку. Які надра зацікавили Трампа і що може дати Україна? 11 лютого https://epravda.com.ua/biznes/shcho-vidomo-pro-ridkisnozemelni-metali-ta-chomu-voni-zacikavili-svit-803063/

15. Андрій Кадук. У Китаї виявили нове велике родовище рідкоземельних металів: чим вони цінні. 19 січня 2025 https://focus.ua/uk/technologies/689147-u-kitaji-viyavili-nove-velike-rodovishche-ridkozemelnih-metaliv-chim-voni-cinni

16. Christopher McFadden. Сhina hits jackpot, finds 1.15 million ton rare earth mineral deposits in Yunnan. Jan 18, 2025 https://interestingengineering.com/science/china-rare-earth-mineral-deposits-yunnan

17. China’s Rare Earth Dominance and What It Means for the World https://www.zimtu.com/chinas-rare-earth-dominance-and-what-it-means-for-the-world/#:\~:text=China%20controls%20the%20global%20supply,these%20critical%20elements%20are%20indispensable.

18. China's rare earth exports in 2024 climb as home demand limited January 13, 2025 2:35 AM https://www.voanews.com/a/china-s-rare-earth-exports-in-2024-climb-as-home-demand-limited/7934585.html

19. China’s Grip On Rare Earth Elements Loosens https://carboncredits.com/chinas-grip-on-rare-earth-elements-loosens/

20. Mathieu Xémard China has a monopoly on rare earth metals. January 29th, 2025 https://www.polytechnique-insights.com/en/columns/geopolitics/china-has-a-monopoly-on-rare-earths/

21. Китай национализирует все запасы редкоземельных металллов, которые используются в производстве чипов. 02 Июля 2024 https://www.cnews.ru/news/top/2024-07-02_kitaj_natsionaliziruet_zapasy

22. Jason Mitchell. China’s stranglehold of the rare earths supply chain will last another decade. 26 April, 2022 https://www.investmentmonitor.ai/sectors/extractive-industries/china-rare-earths-dominance-mining/?cf-view

23. Анна Королева. Редкоземельные элементы могут стать действительно редкими. 17 октября 2024 https://monocle.ru/2024/10/17/redkozemy/

24. Редкоземельные металлы России. 2022 год. Государственный доклад «О состоянии и использовании минерально-сырьевых ресурсов Российской Федерации в 2022 году». https://nedradv.ru/nedradv/ru/resources?obj=ab05b068239ede80d3dd35cf406b4000

25. Health risk assessment of rare earth elements in cereals from mining area in Shandong, China. 29 August 2017 https://www.nature.com/articles/s41598-017-10256-7

26. China Northern Rare Earth builds its largest project in Zibo, with polishing powder output expected to be highest in the world. By Global Times. Oct 25, 2022 https://www.globaltimes.cn/page/202210/1277900.shtml

27. The 5500 t / a rare earth separation project of Shandong Shenghe New material Technology Co., Ltd. is about to be relocated to the park. Nov 26, 2020. Department of Industry and Information Technology of Shandong Province https://news.metal.com/newscontent/101327801/The-5500-t-a-rare-earth-separation-project-of-Shandong-Shenghe-New-material-Technology-Co-Ltd-is-about-to-be-relocated-to-the-park

28. China's domestic market needs for rare earth materials https://chinapower.csis.org/china-rare-earths/

29. Milton Ezrati. How Much Control Does China Have Over Rare Earth Elements? Dec 11, 2023 https://www.forbes.com/sites/miltonezrati/2023/12/11/how-much-control-does-china-have-over-rare-earth-elements/

30. Selcan Hacaoglu and Firat Kozok. Turkey Seeks Chinese Partnership on Rare Earth Elements for EVs. September 03, 2024 https://www.bnnbloomberg.ca/investing/commodities/2024/09/03/turkey-seeks-chinese-partnership-on-rare-earth-elements-for-evs/

31. China’s Sept rare earth exports curbed by rising domestic demand, prices. Reuters | October 14, 2024 https://www.mining.com/web/china-sept-rare-earth-exports-curbed-by-rising-domestic-demand-prices/

32. Rare earth market stirred by price turmoil and waning Chinese dominance https://www.rystadenergy.com/insights/rare-earth-market-stirred-by-price-turmoil-and-chinese-dominance

33. Алекс Будрис. Их импортозамещение: как Запад пытается потеснить Китай с рынка редких металлов. 23 декабря 2024. Бизнес https://www.forbes.ru/biznes/527545-ih-importozamesenie-kak-zapad-pytaetsa-potesnit-kitaj-s-rynka-redkih-metallov

35. Китай начал охоту за новыми ценными металлами. Как поиски в Гималаях помогут китайцам обыграть весь мир? 3 июля 2023 https://lenta.ru/articles/2023/07/03/metall/

36. Редкоземельные металлы в России: высокая себестоимость добычи, демпинг Китая. 26 февраля 2025 https://worldmarketstudies.ru/article/redkozemelnye-metally-v-rossii-vysokaa-sebestoimost-dobyci-demping-kitaa/

37. Эксперты заявили об усилении Китаем монополии на рынке редкоземельных металлов. 28 февраля 2025 https://www.interfax.ru/world/1011356

38. Путін заявив, що у РФ більше рідкісноземельних металів і пропонує Трампу добувати їх у "Новоросії". 24 лютого, 2025 https://zn.ua/ukr/usa/putin-zajaviv-shcho-u-rf-bilshe-ridkisnozemelnikh-metaliv-i-proponuje-trampu-spivpratsju.html

39. Imports of rare earth elements saw 30% drop in 2024. 9 April 2025 https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250409-1

40. Joris Teer. Caught in the US-China Crossfire: To Protect Itself, Europe Must Call a Critical Raw Material Emergency. 21.5.2025 https://csds.vub.be/publication/caught-in-the-us-china-crossfire-to-protect-itself-europe-must-call-a-critical-raw-material-emergency/

41. Melissa Pistilli. Top 10 Countries by Rare Earth Metal Production. Mar. 25, 2025 https://investingnews.com/daily/resource-investing/critical-metals-investing/rare-earth-investing/rare-earth-metal-production/